Промо на dev.uaMoney

10 March 2026, 10:45

2026-03-10

MFIs in Ukraine: what they are, how they work and how to protect yourself

Microfinance organizations in Ukraine provide small, short-term loans, mostly online and through a simplified procedure. Despite the speed of processing, it is important to carefully check the lending conditions, the real cost of the loan, and possible risks before concluding an agreement to protect yourself from financial complications.

Microfinance organizations in Ukraine provide small, short-term loans, mostly online and through a simplified procedure. Despite the speed of processing, it is important to carefully check the lending conditions, the real cost of the loan, and possible risks before concluding an agreement to protect yourself from financial complications.

Fintech analyst Mykhailo Pochekaitold Channel 24 how microfinance organizations work in Ukraine and what to consider.

What is an MFI?

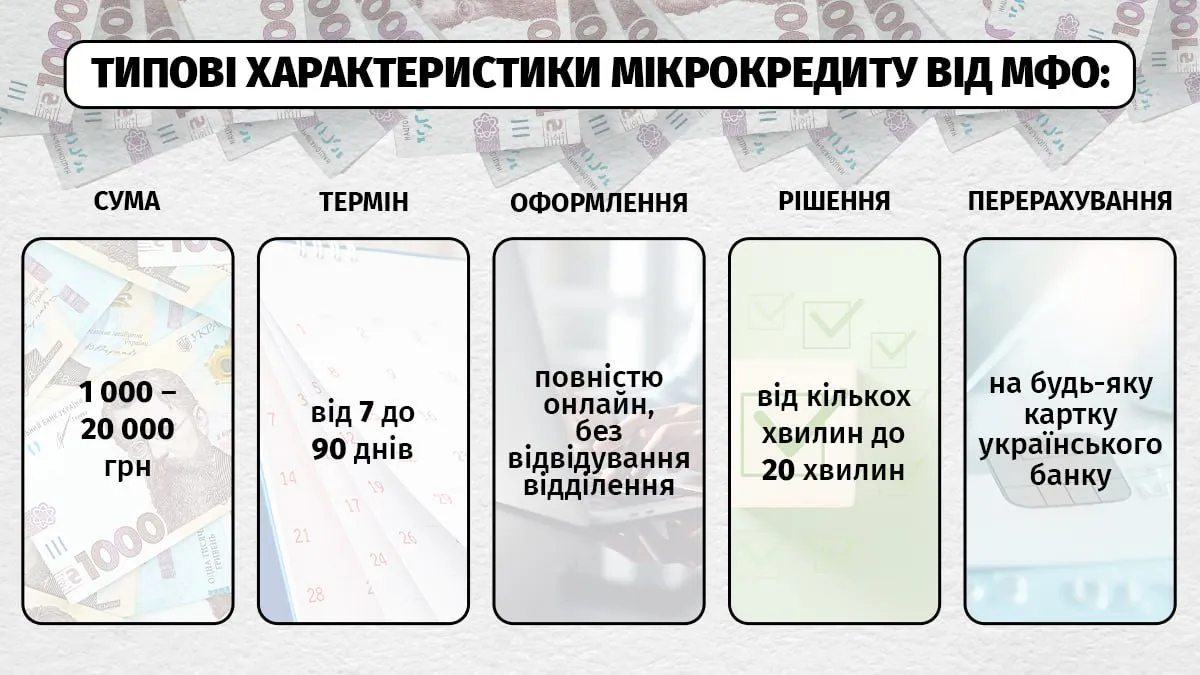

A microfinance institution, or MFI, is a non-bank financial institution that provides short-term loans to individuals for small amounts. Unlike banks, MFIs specialize in so-called microloans: usually from 1,000 to 20,000 hryvnias, with repayment terms ranging from a few days to a few months.

«MFIs are not a „black market“ or „loans“. This is a legal segment of the non-bank financial services market, which fills the niche between bank lending and the complete lack of access to finance. They are especially important for people with atypical employment — freelancers, sole proprietors, seasonal workers,» says Mikhail Pochekai.

Typical characteristics of a microloan from an MFI / Infographics by Channel 24

The decision to issue a loan is made within minutes of submitting the application. According to Mikhail Pochekai, this is possible thanks to fully automated scoring and online verification systems.

What is the legal status of MFIs in Ukraine?

MFIs in Ukraine must operate within the legal framework and are subject to mandatory licensing and state supervision. However, some companies still operate illegally, so it is very important to check the availability of a license before applying.

Until 2020, the regulator of non-bank financial institutions was the National Commission for Regulation of Financial Services Markets, and after its liquidation, all powers were transferred to the National Bank of Ukraine.

According to a fintech analyst, from 2020, MFIs are required to:

have a license or registration with the NBU;

comply with the requirements of consumer protection legislation;

disclose the real cost of the loan (effective interest rate);

comply with the rules for working with personal data.

«The 2020 regulatory reform was an important step for the market. The NBU controls the non-banking financial sector much more strictly compared to the previous regulator. In particular, requirements for rate transparency and a ban on certain aggressive debt collection practices have been introduced. This is not a perfect system, but the direction is right,» notes Mykhail Pochekai.

Why do Ukrainians turn to MFIs?

There is a demand for MFI services in Ukraine, as evidenced by Opendatabot data. According to analysts, in 2025, Ukrainians issued 6.5 million microloans worth 40 billion hryvnias.

There are several reasons for this. First of all, MFIs consider a request in 10-20 minutes online. Such companies use more flexible assessment algorithms and are often ready to issue a loan even with minor past delinquencies. In addition, leading licensed MFIs, such as FirstCredit and LoanPlus, work 24/7. Therefore, people can apply at any time — at night, on weekends, on holidays.

«It is interesting that the demand for microloans during the crisis increases in all countries — this is a global pattern. In Ukraine, the situation is complicated by the combination of a war economy and a pre-war banking infrastructure that has not yet been fully restored in a number of regions. MFIs fill this gap, but it is important that consumers clearly understand the price of such convenience,» emphasizes Mykhail Pochekai.

What are the possible risks and how to avoid them?

Microcredit is an effective tool, but it carries real risks that cannot be ignored. These include:

1. High interest rate

The main risk is the cost of the loan. The daily rate in MFIs can be from 1% to 2,5% per day, and in terms of an annual rate, it is hundreds of percent, says Mikhail Pochekai. At the same time, with prolongation or delay, the debt grows rapidly.

Calculation example / Infographics of Channel 24https://financy.24tv.ua/mfo-shho-tse-take-yak-pratsyuye-ukrayini_n3022097

2. The risk of a «debt trap»

If a person cannot repay a loan on time and takes out a new loan to repay the old one, they fall into a «debt spiral» or «debt pit.» This is one of the most common problems in the field of microcredit. Mikhail Pochekai notes that in this case, loans accumulate and a trap is formed.

Among the reasons why this situation arises, the expert cites significant interest and late payments, so first of all, you need to carefully read the terms of the contract before signing.

By the way, as of early December 2025, Ukrainians owed MFIs over 25 billion hryvnias. In total, the amount of debt increased by 26% over the year.

3. Opaque conditions

Some MFIs hide the real cost of the loan behind small print or complex wording. Always pay attention to the real effective rate (APR), not just the daily interest rate, advises Mikhail Pochekai.

«The promotional rate is not for everyone and not forever. The preferential 0,01% is valid either for a very short time, or only if you return the money exactly on time. If you are late for a day, you automatically switch to the full rate of 1,49% per day. Without warnings,» explains Mikhail Pochekai.

The fintech analyst also advises reading the repayment schedule carefully. According to him, some MFIs build the schedule so that each month a person has to pay only interest, and the entire loan amount must be repaid in one payment at the end.

«For example, 10,000 hryvnias for 12 months can turn into 36,000 hryvnias in interest plus a return of 10,000 hryvnias on the last day. Total — 46,000 hryvnias. If you didn’t read the contract, you didn’t understand the traps,» says Mikhail Pochekai.

«In addition, some MFIs charge a commission at the time of issuance. For example, they charge 5% of the amount. You borrow 10,000 hryvnias — you receive 9,500 hryvnias in your hands, and interest is accrued on all 10,000. The absence of a commission is a real advantage that should be taken into account when choosing an MFI,» he adds.

According to the expert, it is also worth paying attention to the term of the contract. According to him, some MFIs draw up a contract for 5 years, although the loan is issued for 30 days. After the end of the promotional period, they begin to charge not fines, but «regular interest under the contract» — and this is no longer limited by law. Therefore, Mikhail Pochekai recommends always checking both the term of the contract and the loan separately.

How to minimize risks: advice from a fintech analyst

Check the availability of an MFI license on the NBU website

Read the loan agreement in full, including the fine print.

Calculate the full amount to be refunded before signing

Don’t take out a new loan to pay off an old one.

Contact MFIs only when really necessary, not impulsively.

Choose services with a clear and transparent pricing structure

«The main mistake of people who take out a microloan for the first time is that they focus on the amount they receive and do not calculate the amount they have to repay. The advice is simple: always count backwards. How much exactly do you have to repay and on what date? If this amount fits into your budget, the loan is justified. If not, it is better to refuse or take a smaller amount,» notes Mikhail Pochekai.

What rules should be followed when applying to an MFI?

Mikhail Pochekai also explained: for microcredit to solve a problem and not create a new one, it is worth following certain rules: The fintech analyst recommends:

Choose trusted companies

It is worth using the services of MFIs that have an appropriate license from the NBU and a positive reputation in the market. To do this, Mykhail Pochekai advises to review the reviews of real clients, see how many years the company has been operating on the market and whether it is doing so officially.

Gather all information before applying.

You need to prepare your passport, TIN, bank card for verification and active phone number in advance. Errors in the application form may automatically lead to rejection or delay of the decision.

Fill out the questionnaire carefully.

As the fintech analyst pointed out, only reliable data should be provided. MFIs verify information through automated systems, and inconsistencies are quickly detected. In addition, providing knowingly false information can have legal consequences.

Don’t take more than you need.

A credit limit is not a reason to take the maximum. Mikhail Pochekai advises determining the exact amount you need and which you can repay within the specified period. In addition, you can take into account that the smaller the amount and the shorter the term, the smaller the overpayment.

Invest to maturity

Paying on time helps you avoid penalties. If you realize that you won’t be able to make your payments on time, you should contact the MFI in advance and apply for an extension.

«Another important recommendation: keep all documents related to the loan — confirmation of the application, contract, screenshots of correspondence and payment receipts. In the event of disputes, this will be your main argument,» emphasizes Mikhail Pochekai.

What to do if you have problems with microloans?

If a person cannot repay a loan on time, you should not ignore the situation. Mikhail Pochekai recommends that you first contact the MFI from which you took out the loan and ask for restructuring or extension. It is worth doing this before the deadline: most companies are ready to negotiate, because a refund in any form is better than legal costs.

If a company charges unauthorized payments, does not provide information about the debt, or uses illegal collection methods, the fintech analyst emphasizes that a person has the right to contact:

to the National Bank of Ukraine (via the website nbu.gov.ua)

to the National Police (in case of threats or pressure from debt collectors)

to court (in case of unlawful assessment of fines or damages)

The expert also advised checking whether the company is in the NBU register. If not, you should immediately contact the Cyber Police of Ukraine and the NBU.

If the debt has been transferred to collectors

In Ukraine, the activities of debt collectors are regulated by the Law «On Consumer Lending.» According to Pochekai, they do not have the right to threaten, put pressure on relatives, or call at night. In case of such violations, you should contact the police and the NBU.

«The most important thing in a problematic situation is not to panic and not to hide. Silence always worsens the situation: fines are accrued, the case is transferred to court or debt collectors. Proactive dialogue with the creditor is the best strategy. Even small payments and written confirmation of your willingness to repay the debt significantly change the situation in your favor,» adds the fintech analyst.

*LoanPlus provides financial services based on the NBU license No. 21/809-рк dated 12.07.2024. FirstCredit provides services through LLC «FC «ABEKOR». The company’s license was reissued by the NBU decision No. 21/809-рк dated 12.07.2024.