UNIT.City — місце, де люди працюють... КРАЩЕ! Обирай свій простір просто зараз 👉

Марія БровінськаHot News

29 November 2024, 08:45

2024-11-29

UPD. "Dear accountants, sorry for the lost nerve cells." The law on tax increases was published yesterday, but the publication was canceled today. It will come into effect on December 1. What does this mean for taxpayers and employers?

The law on raising taxes, signed by the president on November 28, was published on the same day. This means that it should come into force today, November 29.

However, People’s Deputy Yaroslav Zheleznyak reported that «the publication of the law 11416d on the increase was withdrawn or postponed… in short, it will be published now only tomorrow (11/30), and it will come into force, as planned, from December 1.» This happened, according to the deputy, thanks to publicity. «I will not even comment on the level of chaos in the administration. That’s how you see everything,» Zheleznyak said.

The law on raising taxes, signed by the president on November 28, was published on the same day. This means that it should come into force today, November 29.

However, People’s Deputy Yaroslav Zheleznyak reported that «the publication of the law 11416d on the increase was withdrawn or postponed… in short, it will be published now only tomorrow (11/30), and it will come into force, as planned, from December 1.» This happened, according to the deputy, thanks to publicity. «I will not even comment on the level of chaos in the administration. That’s how you see everything,» Zheleznyak said.

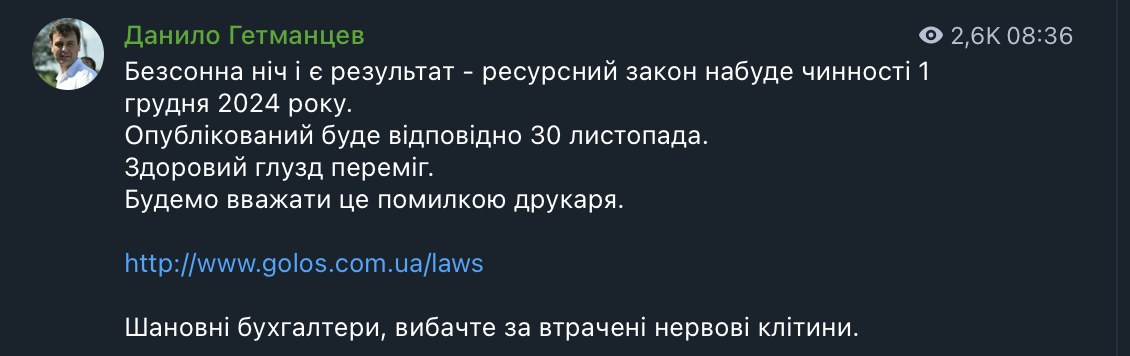

And here’s an apology from Hetmantsev.

In fact, the law means that:

the employer will pay 3,5% more taxes from the official salary. The new law does not apply to personal income tax (PIT), it remains at 18%. The size of the single social contribution (EUS) does not change either — it is at the level of 22%. That is, payroll taxes will not be 19,5% (as now), but 23%. Or 230 hryvnias from each accrued thousand, instead of 195 hryvnias.

The increased military tax rate will apply to the interest income of individuals on deposits. At the same time, it remains at the level of 1,5% for military personnel. It is noteworthy that the rate of 1,5% is applied to income accrued before the entry into force of the new law. That is, for example, the current military levy still applies to the advance in the first half of October.

For individual entrepreneurs of groups I, II, IV of the single tax, a military levy is introduced at the level of 10% of the minimum wage (on the first day of the month). Currently, the minimum is 8,000 hryvnias, so the above-mentioned categories have to pay an additional 800 hryvnias per month in addition to the current taxes. As for the FOP of the III group on the «simplified», a military levy of 1% is introduced for them. Before the new law, they paid 5% of income, that is, now, for example, they have to pay not 50, but 60 hryvnias per month out of every thousand.

From January 1, 2025, monthly reporting on the single social contribution, personal income tax and military levy will be introduced for all tax agents. Quarterly reporting is valid until the end of this year.

The benefits that give the right not to submit a tax declaration on assets and income to those who receive charitable assistance (including from abroad) are continued. This rule applies to internally displaced persons and Ukrainian refugees abroad who receive benefits.

Reporting on the payment of military duty is also being introduced for FOPs. For the first time, they have to submit it in the report for 2024 (starting from October 1).

In relation to gas stations, advance payments from income tax are introduced. They will be fixed, and the size depends on the number of fuel retail outlets and the availability of stores.

For gas stations that do not sell alcohol and/or tobacco products, the advance payment will be 60,000 hryvnias. If only automobile gas is sold — 30 thousand hryvnias. If there are several types of fuel, but gas is 50+%, — 45 thousand hryvnias.

For gas stations where alcohol and/or tobacco products are sold — 80,000 hryvnias. If only autogas is sold as a fuel — 40,000 hryvnias. If there are several types of fuel, but the share of gas is 50+%, — 60,000 hryvnias. The unpaid amount of the income tax advance is subject to a fine.

In addition,income tax for currency exchange points(also in advance) is pegged to the euro. In particular, in the amount of 600 euros in the hryvnia equivalent for cities with more than 50,000 inhabitants (except Kyiv), 700 euros for Kyiv, 200 hryvnias for settlements with up to 50,000 inhabitants

The rent for the extraction of crushed stone, sand and coal is increasing. According to the results of 2024, banks must pay a profit tax of 50%. Income tax for non-bank financial organizations will be 25% as of 2025 (currently 18%).

Increase the minimum tax liability for agricultural producers. Now the minimum amount cannot be less than 700 hryvnias per hectare. And for areas where the share of arable land is 50+% — 1,400 hryvnias per hectare.

Incomes of Ukrainians within the framework of the state program «National Cashback» are exempt from taxation.

Previously, even before the cancellation of the publication, the head of the tax committee, Danylo Hetmantsev, the military levy at the new rate should be withheld only for two days in November. However, how to calculate it, if the salary is accrued for the whole month at once, is still unclear. Hetmantsev promises to publish an official explanation soon.

As for the FOP, according to him, the parliamentarians made a corresponding amendment, according to which the obligation to pay the military tax at the new rates will apply to them from January 1, 2025. But only if the amendment is supported by the Verkhovna Rada next week. «I am convinced: the amendment will be supported,» he noted.

Tax consultant Anton Yanko also made his own analysis of the document, which could enter into force as early as November 29. He notes that a false start with the publication of the document means that:

FOPs of groups 1, 2 and 4 must pay 710 UAH of military duty for October + 710 UAH for November until December 20 (I do not recommend paying yet — see nuance below);

uniformed persons of the 3rd group will pay the military levy from income for the first time for October-December 2024 until February 20, 2025 (or maybe not — see nuance below);

the military tax rate of 5% on SALARY (rent, dividends, income of FOP-generals, etc.) will be applied from 29.11.2024. The main rule here is: EVERYTHING ACCRUED from the date of entry into force (from 29.11.2024) is at a rate of 5%, and ACCRUED BEFORE is at a rate of 1,5%:- full settlement with those exempted up to and including 28.11.2024 is a rate of 1,5%, and from 29.11 — 5%.-

ALL accrued salary for November to employees — at the rate of 5%.

ALL accrued vacation, sick leave, bonuses, etc. in November — at the rate of 5%.

accrued dividends, rent, remuneration according to the CPD (acts dated 28.11.2024 inclusive) — the rate is 1,5%, and from 29.11 — 5%.

«This is my personal version, I do not pretend to be the truth in the last resort and hope for changes and official clarifications. And there is a nuance: the Council must soon adopt a law on changes to these changes (forgive the Lord), but you can wait another 44 days for this law to come into force, so what to do now, unfortunately, everyone has to make their own decision,» he said. .