UNIT.City — місце, де люди працюють... КРАЩЕ! Обирай свій простір просто зараз 👉

Марія БровінськаMoney

12 December 2024, 09:00

2024-12-12

"The lifestyle we have now will be difficult to maintain in old age if nothing is changed now." How do the people in IT prepare for old age without a pension?

PR Manager at Pingle Game Studio Yulia Tugolukova is 33 years old. And already a year ago, the girl started saving for her future pension.

«I regret that I did not do this earlier, just as I did not deal with the issue of my savings in principle. «Over the past year, my behavior model has changed significantly: I started to take a deeper interest in this topic, I took several online courses on financial literacy,» the girl says.

Julia gradually came to the realization that the current lifestyle will be difficult to maintain in old age if nothing is changed right now.

«By the way, you can check your projected pension on the website of the Pension Fund of Ukraine. It is 10,000 hryvnias per month for me — certainly not the smallest, but it is still a pittance compared to my current monthly expenses,» says the specialist.

Yuliya has been regularly replenishing her account in the non-state pension fund «Dynasty» for a year now. In addition, he has an OVDP and regularly buys foreign currency. «I put aside 10 to 20% of my income in total. I reinvest all the income, and it conditionally goes to retirement,» says the PR woman.

Yulia plans to open a brokerage account and start investing in shares of foreign companies, since the yield there is much higher than that of instruments available in Ukraine.

Such a responsible approach to securing one’s future is not surprising. After all, the Ministry of Social Policy recently announced yet another new approach to pension provision, which may begin to operate as early as 2025.

dev.ua conducted a survey among IT professionals on how they take care of their secure old age. We present the results.

PR Manager at Pingle Game Studio Yulia Tugolukova is 33 years old. And already a year ago, the girl started saving for her future pension.

«I regret that I did not do this earlier, just as I did not deal with the issue of my savings in principle. «Over the past year, my behavior model has changed significantly: I started to take a deeper interest in this topic, I took several online courses on financial literacy,» the girl says.

Julia gradually came to the realization that the current lifestyle will be difficult to maintain in old age if nothing is changed right now.

«By the way, you can check your projected pension on the website of the Pension Fund of Ukraine. It is 10,000 hryvnias per month for me — certainly not the smallest, but it is still a pittance compared to my current monthly expenses,» says the specialist.

Yuliya has been regularly replenishing her account in the non-state pension fund «Dynasty» for a year now. In addition, he has an OVDP and regularly buys foreign currency. «I put aside 10 to 20% of my income in total. I reinvest all the income, and it conditionally goes to retirement,» says the PR woman.

Yulia plans to open a brokerage account and start investing in shares of foreign companies, since the yield there is much higher than that of instruments available in Ukraine.

Such a responsible approach to securing one’s future is not surprising. After all, the Ministry of Social Policy recently announced yet another new approach to pension provision, which may begin to operate as early as 2025.

dev.ua conducted a survey among IT professionals on how they take care of their secure old age. We present the results.

What will be the pension system of the future

As previously reported by dev.ua, the Ministry of Social Policy published a draft law that provides for the reform of the solidarity level of the pension system. According to the document, pension payments will consist of basic and insurance components. Accumulated pensions have also been announced.

The basic pension will be mandatory and the same for all pensioners, providing a basic level of social protection. Its amount will be 30% of the minimum wage after taxes.

If the pension reform becomes operational in 2025, the amount of the basic pension will be UAH 1,848 (minimum salary — UAH 8,000, and after paying personal income tax and the new military levy — UAH 6,160).

The insurance component will depend on the length of service and salary and will be calculated according to the points system. The calculation of the insurance component within the framework of the reform will be significantly updated: instead of cumbersome formulas, a point system will be introduced, numerous allowances and «extensions» (surcharges so that the amount of payments equals the living wage guaranteed by the Constitution) will disappear, and special pensions will generally be removed «by the brackets» of the solidarity level.

The value of one pension point will be revised every March, depending on the average salary in the country, replacing the traditional indexation of pensions.

The number of their enrollments will depend on the amount of salary. If it is equal to the average official salary in Ukraine (according to the data of the Pension Fund), then a person is awarded 10 points for a month of work.

If the amount of the reward exceeds the average salary in Ukraine, the number of points increases proportionally. And vice versa — if it is smaller, then the points will be proportionally less.

Since it is necessary to have at least 35 years of work experience to take a well-deserved rest, a person who has received an average salary throughout his life will earn 4,200 points. This number will turn into a kind of benchmark that will be used to calculate the value of one point. The minimum number of them, which will give the right to receive payments according to age (with the necessary experience) is 1440 points.

The value of the pension point will be calculated once a year. For this, the product of the average salary for the previous year and the coefficient of 0.3 will be divided by 4200. For example, for 2024, the value of the pension point calculated according to this formula would be approximately UAH 1.02.

In order to calculate the amount of the insurance pension payment, you need to multiply the number of earned points by the value of one.

To retire at the age of 60, it will be necessary to have at least 35 years of work experience. If you have 15 years of experience, you can receive a pension at the age of 65.

At the same time, the state will make it possible to retire to persons who at the age of 65 do not have enough work experience, but have accumulated a certain number of points (more on them below).

The draft law provides that changes to the pension system will enter into force on July 1, 2025 .

If the plan of the Ministry of Social Policy succeeds, a three-level pension system will work in Ukraine, and in old age Ukrainians will be able to claim payments, the amount of which will exceed half of their salary.

After the reform, the amount of payments to those people who are already retired will be calculated according to the new rules, that is, taking into account the points earned by them in the past. Also, a basic pension will be added to their insurance payment.

Other additional payments — for a certain status of a person or special working conditions — will be withdrawn from the pension system and transferred to the state budget.

It is expected that after the reform, the amount of solidarity pensions will increase for 80% of Ukrainian pensioners. If the pension calculated according to the new rules turns out to be smaller than before, its amount will not be reduced.

Another part of the reform is the introduction of a mandatory accumulation level of the pension system. A feature of the second level is the individual nature of contributions. If at the solidarity level, payments are made from the «common cauldron» into which contributions are made by citizens of working age, then at the accumulative level, the amount of future payments depends solely on how much a person has saved for old age.

Within the framework of the reform, individual pension accounts will be opened for every working Ukrainian, which will be replenished monthly by employers and the state. An accumulation fund that will manage these funds will invest them in order to protect against inflation and multiply.

Starting from the fourth year, citizens will have the right to transfer their pension savings to the accounts of private companies that are authorized to participate in the second level. These can be non-state pension funds (NPF), life insurance companies or banks. The cumulative level of the pension system is planned to be introduced from January 1, 2026.

How the IT people take care of a safe old age

According to the results of the dev.ua survey, almost half of the surveyed IT workers are already preparing for retirement and taking steps towards a secure old age. More than 40% of respondents are only thinking about it.

Are you preparing for retirement?

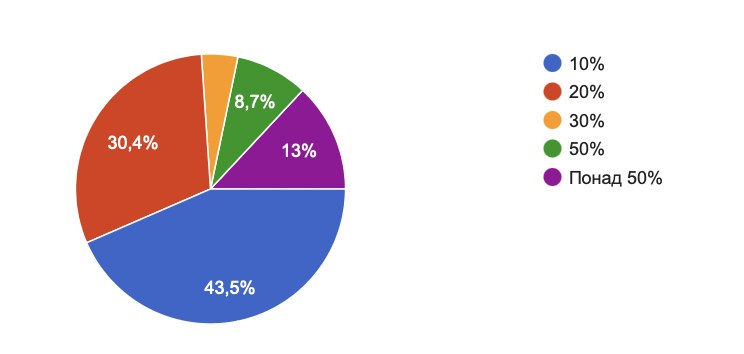

For the most part, IT people are ready to save 10–20% of their earnings. But there are also those who can save even half of the earned money.

How much of your income are you willing to save in order to live comfortably in old age?

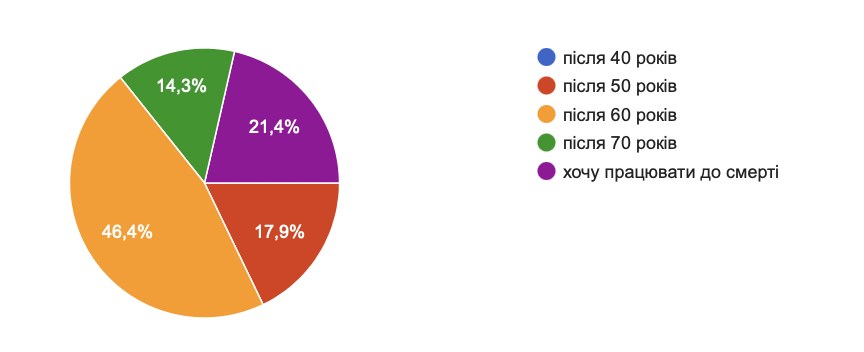

And interestingly, most of the IT people are ready to retire no earlier than 60 years old. However, there are many who plan to work for the rest of their lives.

At what age do you plan to retire and not work?

How IT worwers are preparing for retirement

dev.ua asked IT people to tell about their experience of preparing for a secure old age. Here are the most popular options professed by IT professionals.

Investing in real estate and renting it out.

Investments in currency.

Investment in IVV.

Investing in cryptocurrency.

An account in a non-state pension fund and regular top-ups.

Invest in ETFs through Interactive Brokers.

Starting your own business with constant income.

It is interesting that among the plans of the citizens of IT workers for a safe old age there are also other plans, in particular, some plan to go abroad for any purpose and meet favorable years not in Ukraine.

Also among those interviewed are representatives of the FIRE philosophy (financial independence retire early), who plan to retire much earlier than 60 years old. Interestingly, according to the DOU, only 5% of IT workers adhere to this concept. However, the idea seems interesting: among those who are familiar with it, 15% chose it, and another 41% would like to do it.

«I invest in the stock market through Interactive Brokers, I buy ETFs, not individual stocks. I started recently, but every month I save a significant part of my income in order to reach financial freedom sooner, approximately in 15 years when I will be 50. You can say that I follow FIRE, I save more than 70% and try to live frugally. I don’t expect much from the state pension,» says one of the experts on condition of anonymity.

And here is another feedback about the FIRE experience from a 31-year-old developer: «I am convinced that there will be no support from the state at the time of my retirement. There will be no pension provision as such. And I already expect that the state will be able, if not to provide for me, at least to support me. That’s why I try to take care of my adult years as much as possible now — I work hard, save money, try to invest in order to preserve capital. So far, everything is going according to plan. But life is confusing, so I’m looking at a wide range of investment instruments in order to preserve savings.»

What do IT workers invest in?

To earn passive income now and have a safe old age, IT people often diversify their portfolios by having several investment vehicles.

Ivan Burban, Head of Marketing Coupler.io at Railsware believes in the FIRE philosophy.

First and foremost, FIRE is about financial freedom, not early retirement

No one will kick you out of the conditional FIRE club if you will work at 46, but at the same time you will have passive income. It is the aspect of independence that is important to me personally — work not only for the sake of money, but also for interesting projects and personal growth. And, of course, the opportunity to have time for family, hobbies, health, etc. In addition, during a full-scale war, the best investment in «calm old age» is an investment in the Armed Forces. I cannot say that I am an exemplary representative of the FIRE current, but many steps in this direction have already been taken. In particular, at the beginning of his career, he started investing in ETFs, non-dividend assets, bonds, etc. It makes sense to diversify your investments between different types of assets in order to reduce risks and have a more predictable and stable income. On the one hand, compound interest is a cool thing that everyone should use. On the other hand, in the IT industry, the surest path to financial freedom is building your own business or working for a company with real options. In which direction can you still look? Traditionally, for real estate for rent. In Ukraine, especially in large cities, it can be an attractive investment even under current conditions. It is unlikely that you will find another country where the payback of residential real estate is about 10 years? On the other hand, a number of experts recommend looking in the direction of commercial areas, but I have not yet entered this industry. Therefore, the conditional «package» of real estate+ETF+bonds on Interactive Brokers is already a good retirement plan. What else is important not to forget in your FIRE program? The presence of «free» money does not cancel financial literacy — you need to understand how various tools work and constantly update your knowledge. Controlling your own expenses and smart budgeting, at the same time, will allow you to expand your investment potential. And a couple of other important things. FIRE is a marathon, not a sprint, so don’t expect quick results. And, after all, financial independence is not an end in itself, it is a way to have a lifestyle that is comfortable for you.

dev.ua talked about the experience of Senior Software Engineering Manager at GlobalLogic Taras Kuprunets, who chose the purchase of ETF securities as his main type of investment. For this, he uses the site of the brokerage firm Interactive Brokers.

Why ETF? The widest possible market and diversification

If we talk about shares, then these are instruments with fixed income. I cannot accurately predict my earnings, unlike the same bank deposit. But if you, for example, bought shares of conventional Apple, Tesla or Microsoft in 2008, then in 10 years they could increase in price at least several times. This is the main financial motivation. There are also dividends for these shares, but in my case they do not significantly affect the result.

The ETF financial instrument consists in the fact that it actually contains the entire world market piece by piece. It is very dynamic: someone increases in capitalization, someone is pushed out. For example, you would like to buy Tesla shares, because at some point they are growing strongly. But Elon Musk, conditionally, burned out with some project, and the shares went down. You started losing money because stocks have high volatility. In order to somehow protect yourself, you need to conditionally buy Microsoft shares. And it is also desirable to invest not only in technological companies, but also in some raw materials companies, for example, oil companies.

Therefore, optimal smart diversification is a tool of stability. But if you yourself buy individual shares of individual companies, it is difficult and costly. You attract a broker every time and pay him a commission. Every year you have to rebalance, buy something, sell something to even out the balance. These are again expenses — commissions. That is why, in fact, funds that balance these processes, such as Vanguard, have emerged. So you have, for example, the best 500 companies collected in one ETF. This is the widest possible market and optimal diversification for you.

Oleksandr Omelaenko, Project Lead of Unreal Department at Pingle Game Studio, chose OVDP as his main type of investment.

Currently, OVDP is almost an ideal tool for a beginner

At the same time, it should definitely make up a significant portion of the investment shark’s portfolio. Advantages of OVDP: high liquidity — money can be withdrawn from investments in a few days very low risks — almost zero chance of losing everything. In the worst case, the devaluation of the hryvnia threatens profitability — in the current state, OVDPs have a fairly high rate of convenience — the income of OVDPs is not subject to taxes. Maybe this will change in the future, but now it’s really convenient.

Of course, I considered and continue to consider other options. Unfortunately, for most of the really interesting tools, it is necessary to withdraw funds abroad, and this is now a very big problem. From long-term investments with low risks, you should definitely pay attention to the S&P500 — in the future, I intend to keep the main part of the portfolio there. However, there are also investment instruments available in Ukraine with different «risk/return» ratios. You can invest in real estate — and it is about both the purchase of your own and participation in compatible projects. There are programs with car leasing, etc.

Maryna Syrovets, Java Developer, believes that real estate investment is the most understandable way of passive income.

It is possible to deal with real estate on your own, but it is exhausting both morally and financially. That’s why part of my investment strategy is looking for REIT companies.

The Binaryx platform offers a new flexible approach to distributed real estate ownership with a very low entry threshold and provides excellent diversification within the project. I started investing with a minimum of $50, now I have more than $10,000 in various projects. The platform provides an opportunity to invest not only in ready-made real estate in different countries, but also in construction. Investments in construction are usually more profitable, but do not bring monthly dividends. I started making money investing in a tokenized investment virtually immediately. Profit is distributed during the month with the possibility of withdrawal at any convenient time.

In 2025, they plan to introduce changes to the calculation of pensions. What are pension points, how will accumulated pensions work and how will it affect the amount of benefits for existing pensioners

«Innovation alone is not enough to attract investment.» Why are Western investors in no hurry to invest in Ukrainian miltech, which is experiencing its best time

Ukrainian IT workers co-invest in real estate in Bali, Turkey and Montenegro and earn on Airbnb. How to become a co-owner of a house abroad with a starting capital of $50?